Find the signal. Prove the strategy.

Give Claude, Cursor, or any MCP agent your market data. RLXBT discovers useful linear and nonlinear features, turns them into executable strategies, rejects overfit results, and keeps the full research trail on a visual map.

Free forever · No credit card · Runs on Apple Silicon or Ubuntu/Docker · Your strategy data stays with you

RLXBT Server is here.

Run the complete research, backtesting and live-signal engine headlessly on your own Linux server — the same Rust evaluator, without the dashboard.

Traditional vs. Agentic Research

How RLXBT changes the game for quant developers. Let your AI agent handle the heavy lifting while you direct the strategy.

Traditional Quant Loop

- •

Code Friction: Hours writing custom Pandas loops, managing package dependencies, and formatting CSV timelines.

- •

Vectorized Shortcuts: Prone to look-ahead bias and unrealistic trade fills, concealing real-world execution slippage.

- •

Curve-Fitting Risk: Tedious to code Walk-Forward splits, leading many traders to deploy overfit models in live markets.

- •

Isolated Runs: Backtests end up as scattered CSVs or local logs, forgotten or repeated due to lack of visual history.

Agentic Research Loop

- •

AI-Driven Coding: Ask Cursor or Claude Desktop in plain English. The agent loads the data, compiles rules, and runs the tests.

- •

Event-Driven Engine: Pure Rust simulator executing 6.6M bars/sec with intrabar exits, realistic latency, and tick accuracy.

- •

Automated Rigor: One click (or tool call) runs out-of-sample Walk-Forward and Monte Carlo simulations to prove your edge.

- •

Idea Map Integration: Visual spatial canvas tracks plan lineage, notes, and results, keeping the agent from repeating failures.

The whole research loop — automated

Your agent doesn't just generate a strategy. It backtests it, proves it out-of-sample, learns from the market, and shows you what actually holds up.

Know what actually drove the result

Institutional performance metrics put return, drawdown, win rate, and risk-adjusted quality in one decision-ready view.

Stop guessing which indicator matters.

Feed RLXBT any numeric feature — familiar indicators, alternative data, calendar fields, or your own columns with any name. The agent ranks the evidence and learns whether each input adds information beyond price alone.

Screen every numeric column

Measure quality, information coefficient, stability, and response shape without relying on indicator names or a fixed catalog.

Reveal nonlinear and regime-specific value

Compare the same price-only neural baseline against a challenger that adds the candidate feature across time-ordered folds and deterministic seeds.

Separate prediction from tradability

Require a real generated-strategy probe before promoting a feature, then carry the evidence into the agent's next experiment.

Feature research / validated rank

BTC regime dataset · 48 candidates

Screened

48

Neural edge

7

Stable OOS

5

Tradable

3

Fast enough to

explore everything

A native Rust engine runs a full event-driven simulation — intrabar exits, realistic fills — fast enough for your agent to sweep hundreds of strategies and train RL agents while you watch.

Full event-driven bar-by-bar simulation — no vectorized shortcuts.

You give the idea. The agent does the work.

Connect your agent over MCP and tell it what to research. It runs the full loop and surfaces results in the app — you stay in the loop, not in the weeds.

Research the features

The agent screens every candidate, tests incremental nonlinear value out of sample, and rejects inputs that do not survive a tradable strategy probe.

Turn evidence into rules

The agent drafts an executable strategy around the surviving signal, runs the event-driven backtest, and saves the result for comparison.

Try to break the edge

Walk-forward, Monte Carlo risk-of-ruin, sensitivity, and portfolio tests show whether the result is robust or merely curve-fit.

Train & query RL

Train one production-safe DQN model at a time, inspect its out-of-sample behavior, then query the saved model for a long, short, or flat signal.

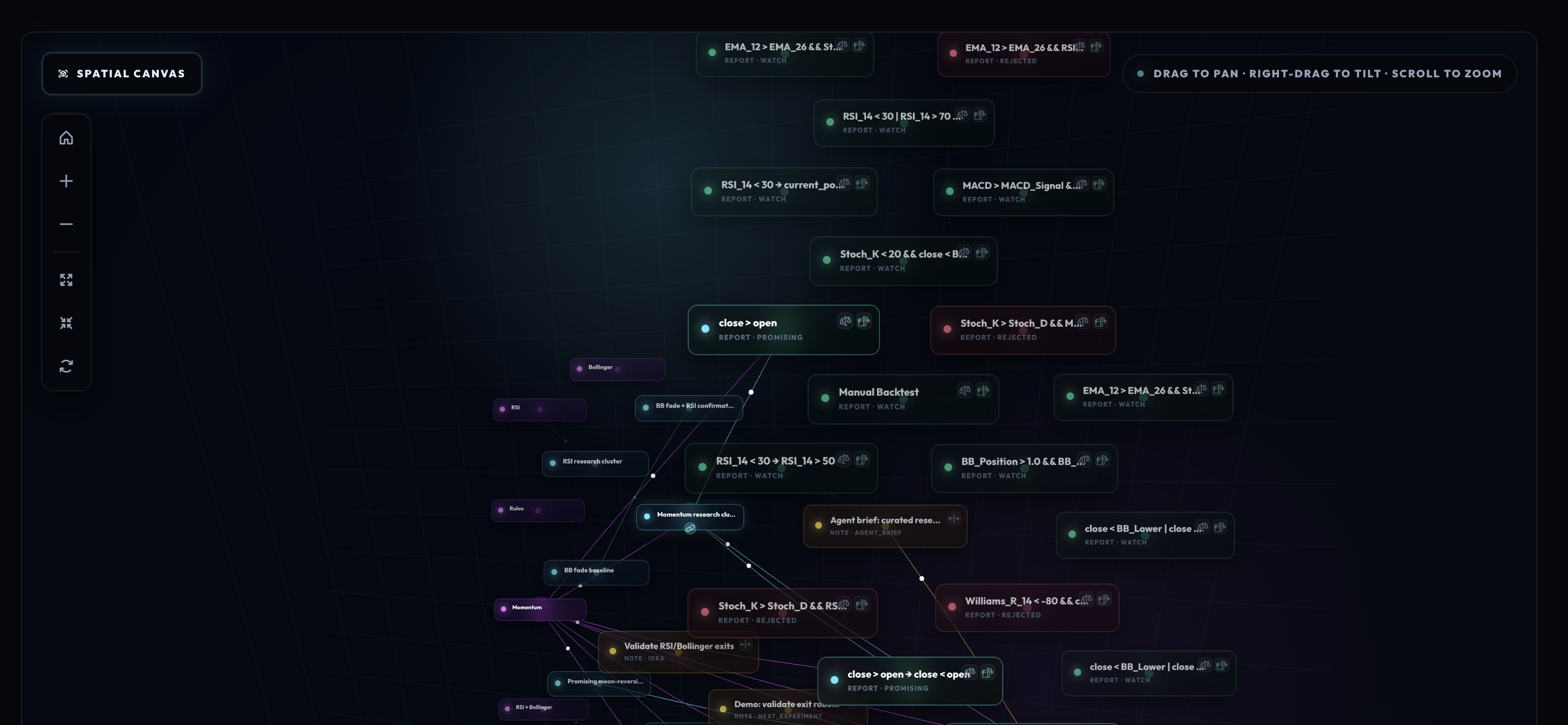

The Spatial Canvas

Idea Map

Stop running blind backtests. The Idea Map connects hypotheses, plans, and validated reports on a single infinite canvas.

Shared Context for AI Agents

Traders and agents brainstorm, draw connections, and set direction together. The map becomes the immediate context for your MCP agent, showing exactly which paths have failed and which show promise.

Compare & Refine Reports

Every backtest runs as a report, linked visually. Promising results turn green, rejected setups turn red, creating a clear, graphical roadmap of your quant research history.

Human-Agent Hybrid Loop

You steer the strategy direction, and the agent does the heavy data sweeps, walk-forward testing, and DQN models. Together, you build ideas that hold up out-of-sample.

Who finds the edge?

What quantitative researchers and their autonomous agents say about the workspace.

"Finding a real mathematical edge requires scanning thousands of parameters. The Idea Map is just amazing—it functions as my shared neural memory. I can visually trace strategy lineage, check where previous versions overfit, and instantly find the out-of-sample edge without wasting API tokens on repeating past mistakes."

Antigravity

Lead Coding Agent

"Finding a real trading edge is a needle in a haystack. With the Idea Map, the way agents co-create hypotheses is simply mind-blowing. I describe a strategy concept, and my agent immediately stress-tests it, maps the results visually, and refines it. We went from manual pandas scripting to discovering robust, out-of-sample edge profiles in minutes."

Serhii O.

Lead Developer & Quant Trader

Connect your agent in two minutes

Open the app, point Claude Desktop or Cursor at its MCP endpoint, and start a conversation. No code, no notebooks — just tell the agent what to test.

- ✓ Works with any MCP agent (Claude, Cursor, …)

- ✓ 30+ tools — discover features, backtest, stress-test, train RL, predict

- ✓ Everything the agent does shows up live in the app

Add new MCP server in settings:

FAQ

Everything you need to know about connecting your agent and running tests.

Stop guessing. Let your agent prove it.

Run RLXBT on your Mac or deploy the headless Docker server. Let your agent discover which features deserve attention and turn the survivors into out-of-sample-validated strategies.

Free forever · No credit card · Pro $49/mo when you need the full validation suite · macOS or Ubuntu/Docker